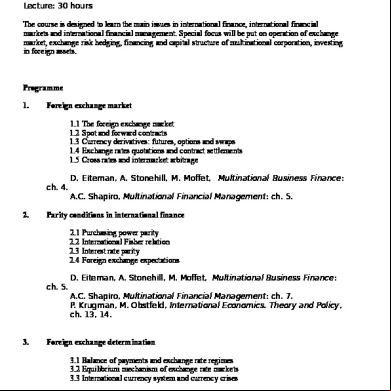

11.30 Michel Folliet, International Finance Corporation 3l2a2z

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 3b7i

Overview 3e4r5l

& View 11.30 Michel Folliet, International Finance Corporation as PDF for free.

More details w3441

- Words: 1,797

- Pages: 11

IFC experience in financing and advising cement companies in emerging markets Michel Folliet, IFC Global Manufacturing Cemtech Conference, Dubai March 6, 2011 1

CONTENTS

-

IFC AT A GLANCE

-

IFC IN THE CEMENT SECTOR

-

IFC PROJECT TRANSACTION CYCLE

-

Q&A

2

1

IFC: Our Reputation and Value • IFC is the world’s largest multilateral private sector investor in the emerging markets.

• Total Committed Portfolio: US$49 Billion at June 30, 2010 • AAA rating • 3,350 employees in 86 countries worldwide (55% in the field) • In-house syndications department working with over 200 banks • Strong advocate and brand on environmental and social issues • Climate Change mitigation is a key priority for IFC/World Bank • Political risk mitigation • Preferred creditor status

3

FY 2010 IFC Investments by Industry Commitments for IFC’s : US$12.7 Billion Additional Resources Mobilized: US$5.4 Billion Private Equity and Investment Funds 3%

Subnational Finance 1%

Oil, Gas, Mining and Chemicals 8%

Agribusiness 4% Global Financial Markets 53%

Infrastructure 12% Health and Education 3%

Global Manufacturing and Services 11%

Global Information and Communication Technologies 4%

4

2

FY 2010 IFC Investments by Region US$2.4 billion in Sub-Saharan Africa US$1.5 billion in Middle East and North Africa Middle East and North Africa 12%

Global 1%

Sub-Saharan Africa 19% East Asia and the Pacific 12%

Latin America and the Caribbean 24%

Europe and Central Asia 23%

South Asia 8%

5

IFC ADVISORY SERVICE Total Spending in FY 2010: $268 Million

Access to finance

Sustainable Business

IFC helps to increase the availability and affordability of financial services, particularly to micro, small, and medium enterprise clients.

Building on IFC’s environmental and social performance standards, we promote sustainable business practices among firms in infrastructure, extractive industries, manufacturing, agribusiness, and services.

Portfolio of 238 projects in 68 countries, valued at $290 million.

Portfolio of 263 projects in 70 countries, valued at $255 million.

Investment Climate

Public-Private Partnerships

IFC helps governments implement reforms to improve their business environment and encourage and retain investment, thus fostering competitive markets, growth, and job creation.

IFC advises governments on structuring public Private partnership transactions in infrastructure and other public services.

Portfolio of 144 projects in 67countries, valued at $185 million.

Portfolio of 91 projects in 53 countries, valued at $130 million.

3

IFC offices in Africa Algiers Mediterranean Sea

Rabat

Beirut Jerusalem

Cairo

Amman Dubai

Sana’a

Dakar Ouagadougou Freetown Monrovia

N’Djamena Addis Abala

Abidjan

Accra

Lagos Douala

Nairobi

Kigali

INDIAN OCEAN

Kinshasa ATLANTIC OCEAN Lusaka Antananarivo

Johannesburg

IFC Hubs IFC Country Offices

Maputo

Cape Town

7

IFC IN THE CEMENT SECTOR

8

4

IFC Cement Sector Portfolio of Investments: ÆUS$1.4 billion in 28 companies and 26 countries (30 October 2010) Albania (2) Kazakhstan (1+1) Russia (1) Armenia (1)

Turkey (1) Algeria (1) China (3) Yemen (2) Morocco (1) Egypt (1) Vietnam (1+1) Libya (1) India (2+1) Indonesia (1) Iraq (1) Croatia (1) Bangladesh (1) Laos (1)

Senegal (1) Ethiopia (1) Angola (1) Ghana (1) Mexico (1) Togo (1) Trinidad & Tobago (1) Liberia (1) Dominican Republic (1) Mozambique (1) Paraguay (1) Congo (1) Brazil (1) South Africa (1) Haiti (1)

Blue: Committed Investments Red: Under mandate or strong lead

IFC Cement Portfolio is Composed of Global and Local Clients Over 4 billion US$ invested since inception

Global Clients 53%

Local Clients 47%

9

Recent Transactions (FY2007-FY2010) Inv estment Year

Country

Project Name

Amount US$ million 50

2007

India

OCL

2007

Yemen

AYCC

125

2007

W orld Region

Italcementi

200

2007

Turkey

Sanko Cement

75

2007 2008

Angola

Secil Lobito

China

Tianrui Cement

27 85

2008

Senegal

Vicat-SOCOCIM

26

2008

Ethiopia

Midroc Derba

2008

China

Shanshui III

2009

Albania

Antea - Titan

2009

Algeria

ASEC Algeria

2009 2009

Kazakhstan Vietnam

Jambyl Cement- Vicat Nghi Son II - Taiheiyo

2009

Morocco

Ynna Asment

2010

Africa Region

Heidelberg Africa

180 120

55 110 41 50 175 67 27

2010

Egypt

Titan Egypt

2010

Mexico

Eurus-Cemex

55

2010

India

VicatSagarCement

75

10

5

Selected Cement Sector Transactions Ghana Diamond Cement

Global Italcementi

Ethiopia Midroc

Kazakhstan Vicat/Jambyl Cement

US$6 million Loan, Equity

US$200 million Loan, Equity

US$55 million Loan

US$185 million A/B Loan, Equity

Senegal Vicat-SOCOCIM

Algeria ACC Cement

Mauritania BSA Cimint

Turkey Sanko Cement

US$26 million, Loan US$42 million, IFC Local Currency Bond

US$45 million Loan

US$11 million Loan

US$175 million A/B Loan

Yemen AYCC

Bangladesh Lafarge Surma

Albania Fushe Kruje / Seament

Bosnia and Herzegovina Lukavec / FCL

US$125 million A/B Loan

US$60 million A/B Loan, Equity

US$30 million Loan

US$12 million Loan

Philippines Holcim

Trinidad and Tobago TCL Group

Dominican Republic Domicem

China Anhui Conch

US$27 million Loan, Equity

US$37 million Loan, Risk Management

US$56 million Loan

US$86 million Loan

China Shanshui Cement

China Tianrui Cement

India OCL India Ltd.

Vietnam Nhi Son Cement (Taiheyo)

US$58 million Loan, Equity

US$71 million Loan, Equity

US$50 million

US$56 million A/B Loan

11 Loan

CEMENT SECTOR STRATEGY / PRIORITIES ¾Reinforcing relationship with global players and ing their efforts primarily in high-risk countries, especially in current post-crisis environment ¾Partnering with emerging players developing regionally, promoting South-South investments ¾Focusing on frontier markets which are sufficiently large and are underserved: 50% of IFC’s cement portfolio is in frontier countries ¾Share IFC’s experience and understanding of local business conditions ¾Promoting Environmental and Social high standards ¾Improving energy efficiency and reducing CO2 emission: technology, waste heat recovery, natural gas usage, blended cement and energy efficiency ¾Deal selection is based on project competitiveness (lowest delivered cost producer), IFC sector regional exposure and IFC additionality (developmental impact, energy efficiency and environmental/social performance improvements) ¾Favoring equity and quasi-equity in cement which is appropriate in the current market environment, especially in light of the solid track record of portfolio ¾Maintain consistency (approach and people) and confidentiality

12

6

IFC VALUE ADD AND COMPETITIVE FACTORS ¾

Willing to assume risks through equity/quasi-equity investments

¾

Provide long term financing adapted to the capital intensity and cyclicality of the industry

¾

Syndicate B Loans through extensive banking network, and under the IFC umbrella (preferred creditor status); also leverage our experience to work with DFIs and mobilize DFI loans through new Master Cooperation Agreement

¾

Can play a role in ing a client’s sustainability objectives – potentially a key differentiating factor in the industry.

¾

Help client improve environmental/social performance of its project – compliance with IFC Performance Standards is valued and well regarded by many project stakeholders and other financiers.

¾

Identify and finance energy efficiency initiatives or energy related projects in the sector - e.g. waste heat recovery based power, wind or alternative fuel projects etc.

¾

Contribute to dissemination of international best practices.

¾

Political risk mitigation – e.g., contribute to stability of project agreements with local authorities

13

HOW DO WE PROCESS A CEMENT TRANSACTION?

14

7

IFC: A DEVELOPMENT BANK WITH THE FLEXIBILITY OF A COMMERCIAL BANK Industry and local knowledge & s

Commercial and technical expertise in emerging markets

Sensitivity to government priorities

IFC’s Products and Services Senior Debt • On-lending • Liquidity management • Acquisition financing • Warehousing facilities

Structured Finance

Mezzanine Finance

• Partial credit guarantees

• Convertible debt

• Common shares

• Subordinated debt

• Preferred shares

• Securitization

Private Equity

• Other Tier II instruments

• Bond underwriting

• Syndicated loans

Global Trade Finance Program

Advisory Services

Sustainable Finance

• $2 billion program

• Corporate governance

• Carbon finance

• Guarantees to issuing banks

• Risk management

• Sustainable energy

• 46 issuing banks in 24 countries

• Small and medium business banking

• Supply chain financing

• Housing finance

• Corporate governance financing

• Energy efficiency finance

15

16

Applying IFC Experience: Success Factors Key Success Factors inKey theLessons Cementand Sector Market/Industry Competitiveness Factors ƒ Markets are regional or local in nature with clear regional price differentials, high entry barriers due to capital intensity and expensive transportation/logistical costs. ƒ Careful analysis of import price parity . ƒ Location of facility in relation to the market and raw materials, infrastructure for transportation and assessment of existing or cement capacity ƒ Energy efficiency (40% of production cash cost); best technology ƒ low capital investment cost (in Africa US$125-175/ton cement)

Sponsor Commitment and Values ƒ Due to capital intensive and cyclical nature of the industry, Sponsor’s strong commitment and financial strength are critical to a client’s ability to survive adverse conditions. ƒ Conservative gearing and financial structure for greenfield projects (40-50% equity) ƒ Good governance principles and reputation, and environmental and social commitment sustain economic success.

Sponsor Management and Experience ƒ Experienced management team with good industry and technical knowledge

16

8

A key objective is to minimize the carbon intensity of cement Dealbreakers

Best Practice Technology

• Vertical shaft kiln (“VSK”)

• 5-stage or 6-stage pre-heaters (unless high raw materials moisture)

• Wet kiln or long-dry kiln • Exceptions to the above only if the client commits to close kilns upon commissioning of replacement best practice technology

• Vertical roller mill, Horomill, roller press • Waste-heat recovery power generation • Efficient fans and motors, variable speed drives • Dry-cooled condensers in captive power plants

Benchmarks to limit CO2 emissions to maximum of 650-750 kg/ton cement 1. Maximize Use of Blended Cement ¾ Target: Clinker/cement factor between 0.68 to 0.89 (following local regulations) 2. Minimize Fuel Use in Clinker Production ¾ Target: Fuel use of 2,900 -3,300 MJ/ton of clinker 3. Minimize Use of Electricity in Cement Production ¾ Target: 80 – 105 kWh/ton of cement 4. Encourage Use of Renewable Energy and Alternative Fuels and Raw Materials ¾ Biomass(Jatropha plantations); wind farm; solar

17

IFC: Project Transaction Cycle Early Review

Due Diligence

Negotiation

Disclosure

• Client needs determined

• Assessment of business potential, risks, and opportunities

• Conditions of disbursement and covenants, performance and monitoring requirements, and action plan agreed

• Environmenta l and social information disclosed

• Contribution of project to development assessed • Project screened for potential problems • Site visit • Mandate letter

• Evaluation of financial and economic soundness

• Opportunity for public comment

Internal Approvals and Commitment

• Board consideration • Board approval • Legal review

Disbursement

• Loan disbursed on agreed schedule according to negotiated and conditions

• g of legal documents

• Compliance with IFC’s social and environmental performance standards reviewed

8

9

IFC Customer Profile: Multinationals, Regional and Local

What is important about IFC to a client company? What IFC brings to an investment

Multinational

Regional

Local

Quality stamp of approval Country risk mitigation Exposure to country risk volatility Good s/knowledge Competitive cost

Always

Long tenors

Often Sometimes

Access to local currency funding Complementary funding source

19

THANK YOU QUESTIONS

20

10

Information International Finance Corporation Global Manufacturing, Agribusiness & Services 2121 Pennsylvania Avenue, NW Washington, DC 20433 USA Eric Siew Chief Investment Officer Phone: 1.202.458.9625 E-mail: [email protected]

.

25

11

CONTENTS

-

IFC AT A GLANCE

-

IFC IN THE CEMENT SECTOR

-

IFC PROJECT TRANSACTION CYCLE

-

Q&A

2

1

IFC: Our Reputation and Value • IFC is the world’s largest multilateral private sector investor in the emerging markets.

• Total Committed Portfolio: US$49 Billion at June 30, 2010 • AAA rating • 3,350 employees in 86 countries worldwide (55% in the field) • In-house syndications department working with over 200 banks • Strong advocate and brand on environmental and social issues • Climate Change mitigation is a key priority for IFC/World Bank • Political risk mitigation • Preferred creditor status

3

FY 2010 IFC Investments by Industry Commitments for IFC’s : US$12.7 Billion Additional Resources Mobilized: US$5.4 Billion Private Equity and Investment Funds 3%

Subnational Finance 1%

Oil, Gas, Mining and Chemicals 8%

Agribusiness 4% Global Financial Markets 53%

Infrastructure 12% Health and Education 3%

Global Manufacturing and Services 11%

Global Information and Communication Technologies 4%

4

2

FY 2010 IFC Investments by Region US$2.4 billion in Sub-Saharan Africa US$1.5 billion in Middle East and North Africa Middle East and North Africa 12%

Global 1%

Sub-Saharan Africa 19% East Asia and the Pacific 12%

Latin America and the Caribbean 24%

Europe and Central Asia 23%

South Asia 8%

5

IFC ADVISORY SERVICE Total Spending in FY 2010: $268 Million

Access to finance

Sustainable Business

IFC helps to increase the availability and affordability of financial services, particularly to micro, small, and medium enterprise clients.

Building on IFC’s environmental and social performance standards, we promote sustainable business practices among firms in infrastructure, extractive industries, manufacturing, agribusiness, and services.

Portfolio of 238 projects in 68 countries, valued at $290 million.

Portfolio of 263 projects in 70 countries, valued at $255 million.

Investment Climate

Public-Private Partnerships

IFC helps governments implement reforms to improve their business environment and encourage and retain investment, thus fostering competitive markets, growth, and job creation.

IFC advises governments on structuring public Private partnership transactions in infrastructure and other public services.

Portfolio of 144 projects in 67countries, valued at $185 million.

Portfolio of 91 projects in 53 countries, valued at $130 million.

3

IFC offices in Africa Algiers Mediterranean Sea

Rabat

Beirut Jerusalem

Cairo

Amman Dubai

Sana’a

Dakar Ouagadougou Freetown Monrovia

N’Djamena Addis Abala

Abidjan

Accra

Lagos Douala

Nairobi

Kigali

INDIAN OCEAN

Kinshasa ATLANTIC OCEAN Lusaka Antananarivo

Johannesburg

IFC Hubs IFC Country Offices

Maputo

Cape Town

7

IFC IN THE CEMENT SECTOR

8

4

IFC Cement Sector Portfolio of Investments: ÆUS$1.4 billion in 28 companies and 26 countries (30 October 2010) Albania (2) Kazakhstan (1+1) Russia (1) Armenia (1)

Turkey (1) Algeria (1) China (3) Yemen (2) Morocco (1) Egypt (1) Vietnam (1+1) Libya (1) India (2+1) Indonesia (1) Iraq (1) Croatia (1) Bangladesh (1) Laos (1)

Senegal (1) Ethiopia (1) Angola (1) Ghana (1) Mexico (1) Togo (1) Trinidad & Tobago (1) Liberia (1) Dominican Republic (1) Mozambique (1) Paraguay (1) Congo (1) Brazil (1) South Africa (1) Haiti (1)

Blue: Committed Investments Red: Under mandate or strong lead

IFC Cement Portfolio is Composed of Global and Local Clients Over 4 billion US$ invested since inception

Global Clients 53%

Local Clients 47%

9

Recent Transactions (FY2007-FY2010) Inv estment Year

Country

Project Name

Amount US$ million 50

2007

India

OCL

2007

Yemen

AYCC

125

2007

W orld Region

Italcementi

200

2007

Turkey

Sanko Cement

75

2007 2008

Angola

Secil Lobito

China

Tianrui Cement

27 85

2008

Senegal

Vicat-SOCOCIM

26

2008

Ethiopia

Midroc Derba

2008

China

Shanshui III

2009

Albania

Antea - Titan

2009

Algeria

ASEC Algeria

2009 2009

Kazakhstan Vietnam

Jambyl Cement- Vicat Nghi Son II - Taiheiyo

2009

Morocco

Ynna Asment

2010

Africa Region

Heidelberg Africa

180 120

55 110 41 50 175 67 27

2010

Egypt

Titan Egypt

2010

Mexico

Eurus-Cemex

55

2010

India

VicatSagarCement

75

10

5

Selected Cement Sector Transactions Ghana Diamond Cement

Global Italcementi

Ethiopia Midroc

Kazakhstan Vicat/Jambyl Cement

US$6 million Loan, Equity

US$200 million Loan, Equity

US$55 million Loan

US$185 million A/B Loan, Equity

Senegal Vicat-SOCOCIM

Algeria ACC Cement

Mauritania BSA Cimint

Turkey Sanko Cement

US$26 million, Loan US$42 million, IFC Local Currency Bond

US$45 million Loan

US$11 million Loan

US$175 million A/B Loan

Yemen AYCC

Bangladesh Lafarge Surma

Albania Fushe Kruje / Seament

Bosnia and Herzegovina Lukavec / FCL

US$125 million A/B Loan

US$60 million A/B Loan, Equity

US$30 million Loan

US$12 million Loan

Philippines Holcim

Trinidad and Tobago TCL Group

Dominican Republic Domicem

China Anhui Conch

US$27 million Loan, Equity

US$37 million Loan, Risk Management

US$56 million Loan

US$86 million Loan

China Shanshui Cement

China Tianrui Cement

India OCL India Ltd.

Vietnam Nhi Son Cement (Taiheyo)

US$58 million Loan, Equity

US$71 million Loan, Equity

US$50 million

US$56 million A/B Loan

11 Loan

CEMENT SECTOR STRATEGY / PRIORITIES ¾Reinforcing relationship with global players and ing their efforts primarily in high-risk countries, especially in current post-crisis environment ¾Partnering with emerging players developing regionally, promoting South-South investments ¾Focusing on frontier markets which are sufficiently large and are underserved: 50% of IFC’s cement portfolio is in frontier countries ¾Share IFC’s experience and understanding of local business conditions ¾Promoting Environmental and Social high standards ¾Improving energy efficiency and reducing CO2 emission: technology, waste heat recovery, natural gas usage, blended cement and energy efficiency ¾Deal selection is based on project competitiveness (lowest delivered cost producer), IFC sector regional exposure and IFC additionality (developmental impact, energy efficiency and environmental/social performance improvements) ¾Favoring equity and quasi-equity in cement which is appropriate in the current market environment, especially in light of the solid track record of portfolio ¾Maintain consistency (approach and people) and confidentiality

12

6

IFC VALUE ADD AND COMPETITIVE FACTORS ¾

Willing to assume risks through equity/quasi-equity investments

¾

Provide long term financing adapted to the capital intensity and cyclicality of the industry

¾

Syndicate B Loans through extensive banking network, and under the IFC umbrella (preferred creditor status); also leverage our experience to work with DFIs and mobilize DFI loans through new Master Cooperation Agreement

¾

Can play a role in ing a client’s sustainability objectives – potentially a key differentiating factor in the industry.

¾

Help client improve environmental/social performance of its project – compliance with IFC Performance Standards is valued and well regarded by many project stakeholders and other financiers.

¾

Identify and finance energy efficiency initiatives or energy related projects in the sector - e.g. waste heat recovery based power, wind or alternative fuel projects etc.

¾

Contribute to dissemination of international best practices.

¾

Political risk mitigation – e.g., contribute to stability of project agreements with local authorities

13

HOW DO WE PROCESS A CEMENT TRANSACTION?

14

7

IFC: A DEVELOPMENT BANK WITH THE FLEXIBILITY OF A COMMERCIAL BANK Industry and local knowledge & s

Commercial and technical expertise in emerging markets

Sensitivity to government priorities

IFC’s Products and Services Senior Debt • On-lending • Liquidity management • Acquisition financing • Warehousing facilities

Structured Finance

Mezzanine Finance

• Partial credit guarantees

• Convertible debt

• Common shares

• Subordinated debt

• Preferred shares

• Securitization

Private Equity

• Other Tier II instruments

• Bond underwriting

• Syndicated loans

Global Trade Finance Program

Advisory Services

Sustainable Finance

• $2 billion program

• Corporate governance

• Carbon finance

• Guarantees to issuing banks

• Risk management

• Sustainable energy

• 46 issuing banks in 24 countries

• Small and medium business banking

• Supply chain financing

• Housing finance

• Corporate governance financing

• Energy efficiency finance

15

16

Applying IFC Experience: Success Factors Key Success Factors inKey theLessons Cementand Sector Market/Industry Competitiveness Factors ƒ Markets are regional or local in nature with clear regional price differentials, high entry barriers due to capital intensity and expensive transportation/logistical costs. ƒ Careful analysis of import price parity . ƒ Location of facility in relation to the market and raw materials, infrastructure for transportation and assessment of existing or cement capacity ƒ Energy efficiency (40% of production cash cost); best technology ƒ low capital investment cost (in Africa US$125-175/ton cement)

Sponsor Commitment and Values ƒ Due to capital intensive and cyclical nature of the industry, Sponsor’s strong commitment and financial strength are critical to a client’s ability to survive adverse conditions. ƒ Conservative gearing and financial structure for greenfield projects (40-50% equity) ƒ Good governance principles and reputation, and environmental and social commitment sustain economic success.

Sponsor Management and Experience ƒ Experienced management team with good industry and technical knowledge

16

8

A key objective is to minimize the carbon intensity of cement Dealbreakers

Best Practice Technology

• Vertical shaft kiln (“VSK”)

• 5-stage or 6-stage pre-heaters (unless high raw materials moisture)

• Wet kiln or long-dry kiln • Exceptions to the above only if the client commits to close kilns upon commissioning of replacement best practice technology

• Vertical roller mill, Horomill, roller press • Waste-heat recovery power generation • Efficient fans and motors, variable speed drives • Dry-cooled condensers in captive power plants

Benchmarks to limit CO2 emissions to maximum of 650-750 kg/ton cement 1. Maximize Use of Blended Cement ¾ Target: Clinker/cement factor between 0.68 to 0.89 (following local regulations) 2. Minimize Fuel Use in Clinker Production ¾ Target: Fuel use of 2,900 -3,300 MJ/ton of clinker 3. Minimize Use of Electricity in Cement Production ¾ Target: 80 – 105 kWh/ton of cement 4. Encourage Use of Renewable Energy and Alternative Fuels and Raw Materials ¾ Biomass(Jatropha plantations); wind farm; solar

17

IFC: Project Transaction Cycle Early Review

Due Diligence

Negotiation

Disclosure

• Client needs determined

• Assessment of business potential, risks, and opportunities

• Conditions of disbursement and covenants, performance and monitoring requirements, and action plan agreed

• Environmenta l and social information disclosed

• Contribution of project to development assessed • Project screened for potential problems • Site visit • Mandate letter

• Evaluation of financial and economic soundness

• Opportunity for public comment

Internal Approvals and Commitment

• Board consideration • Board approval • Legal review

Disbursement

• Loan disbursed on agreed schedule according to negotiated and conditions

• g of legal documents

• Compliance with IFC’s social and environmental performance standards reviewed

8

9

IFC Customer Profile: Multinationals, Regional and Local

What is important about IFC to a client company? What IFC brings to an investment

Multinational

Regional

Local

Quality stamp of approval Country risk mitigation Exposure to country risk volatility Good s/knowledge Competitive cost

Always

Long tenors

Often Sometimes

Access to local currency funding Complementary funding source

19

THANK YOU QUESTIONS

20

10

Information International Finance Corporation Global Manufacturing, Agribusiness & Services 2121 Pennsylvania Avenue, NW Washington, DC 20433 USA Eric Siew Chief Investment Officer Phone: 1.202.458.9625 E-mail: [email protected]

.

25

11

Related Documents 3m3m1z

11.30 Michel Folliet, International Finance Corporation 3l2a2z

November 2019 33

International Finance 1l405p

April 2020 33

International Finance 1l405p

November 2022 0

Corporation Finance - Adecco Case 2w1r4j

February 2023 0

International Business Exchange Corporation 364zc

August 2022 0

International Finance Notes.pptx 4a5o6e

November 2019 63More Documents from "Mohd Ali" 4u2v5k

11.30 Michel Folliet, International Finance Corporation 3l2a2z

November 2019 33

What Is Mycrest 5k5o4r

October 2022 0

December 2019 37

Investegatory Project Physics Tesla Coil 164l40

January 2022 0

Alatan Tangan Dalam Kerja Kayu i102z

April 2020 15

October 2019 42